The corporate capital structure highlighted above is a hypothetical structure and for illustrative purposes only. Corporate capital structures may vary substantially from the hypothetical example set forth above.

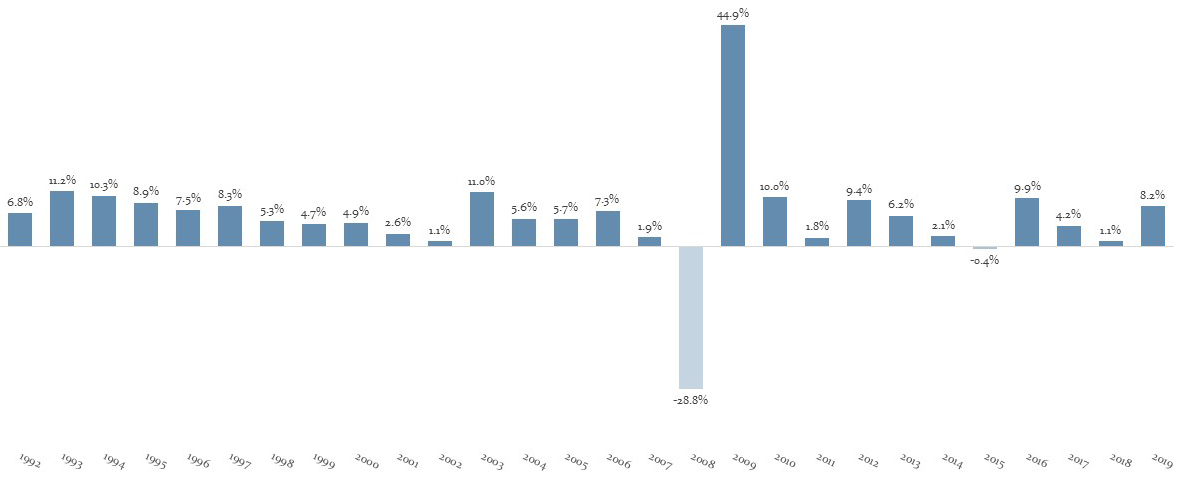

Source:Credit Suisse. Past performance is not indicative of, or a guarantee of, future performance. The Credit Suisse Leveraged Loan Index tracks the investable universe of the US-denominated leveraged loan market. Index returns do not reflect any deductions for fees, expenses or taxes. You cannot invest directly in an index. The Credit Suisse Leveraged Loan Index does not represent the performance of any of the Oxford Funds, and the holdings of the Oxford Funds differ (in terms of both constituent investments and allocations among them) from the holdings of the Credit Suisse Leveraged Loan Index.

The CLO structure highlighted above is a hypothetical structure and for illustrative purposes only. CLO vehicles may vary substantially from the hypothetical example set forth above.